The Home Loan Process

Jeff Hargate

Residential Loan Officer

NMLS# 244491

- 913.787.5164

- 14435 Metcalf Avenue Overland Park, KS 66223

- jhargate@fidelitybank.com

Helping people is a passion for Jeff, whether it is coaching, training, or just lending a helping hand. His compassion for others has been the foundation of his more than 15-year tenure in the banking industry. Jeff has a strong understanding of mortgage lending practices, products and customer needs, and his efforts have earned him ongoing recognition as one of Kansas City’s top loan officers.

Jeff, a graduate of the University of Kansas, also dedicates his time to civil service in an effort to improve the wellbeing of Kansas City metro community members and business owners.

Jeff stands ready to serve his customers with helpful advice and a hassle-free lending experience.

Scott O'Connor

Owner

NMLS# 262654

- (913) 754-1366

- 5350 College Blvd Overland Park, KS 66211

- scott@signaturemortgage.net

Owner, Scott O’Connor has been in the mortgage industry since 1998. After beginning his career in Corporate America he soon realized that his desire to help people would be better served in small business where clients were the focus and not corporate profits. He became a mortgage broker in 2001 and that has been the best decision of his life. Doing what’s best for each individual client, (sometimes that means not doing a loan or sending the client somewhere else), is his driving force in business.

Scott grew up in Leavenworth, KS and received his bachelor’s degree from Cameron University in Lawton, OK where he played college golf. He moved back to Kansas City in 2001 to be closer to family and met his wife Molly. Scott and Molly have a son and daughter, Palmer and Reagan and life revolves around the kids and family. Coaching youth sports is one of Scott’s favorite things to do and he also still enjoys golf, fishing and supporting our great KC Chiefs and Royals.

Scott is an active member of the community with involvement in Nephcure Kidney Internatonal, Harvesters, Head for Cure, St. Jude Children’s Hospital, and Big Brother Big Sister of Greater Kansas City.

Demystifying Home Loans

If you haven’t experienced it before, the home loan process can feel overwhelming, but our agents will help you stay informed throughout the process, from pre-approval to closing. The first thing to do is consult with a mortgage specialist (or two). If you don’t already have someone in mind, we partner with some of the best lenders in the industry, and we’d be happy to introduce you, so you’ll be taken care of.

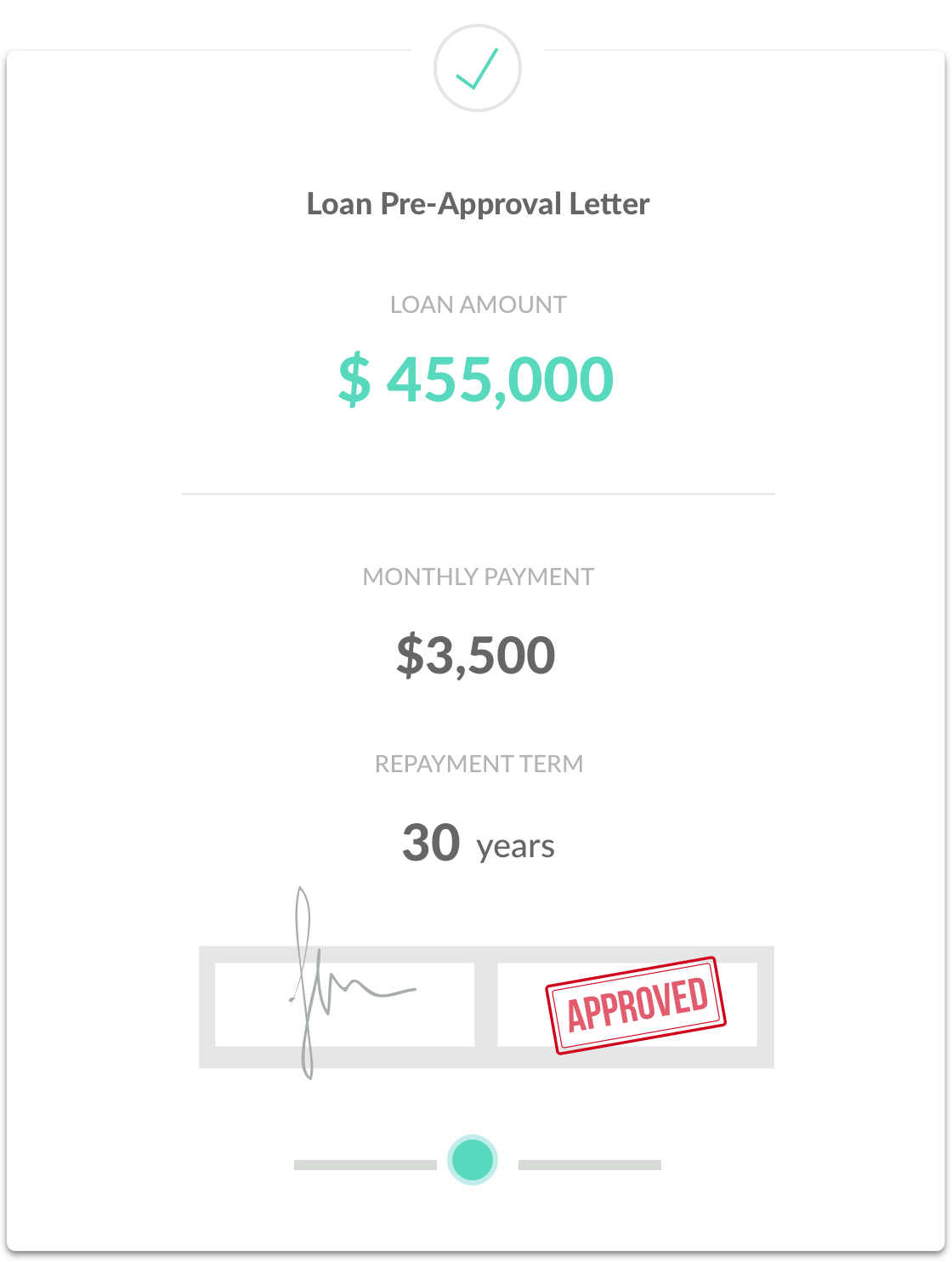

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Loan Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

We Help You Get The Best Loan

Start The Process

We’ll help you find the best local loan officer to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!

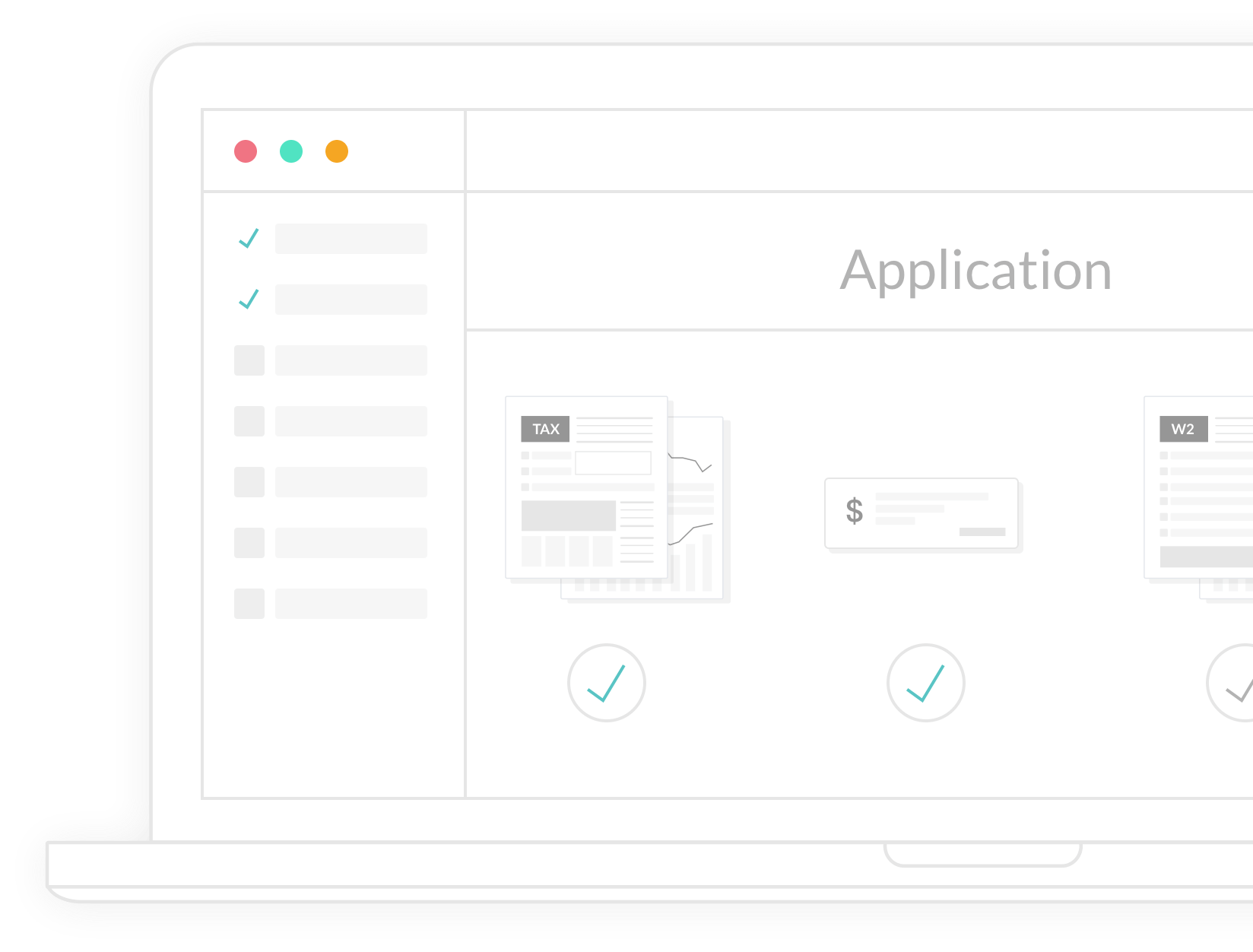

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!